Last Updated on June 19, 2026 by Narendra Sahoo

1️⃣ How Should Businesses Securely Store Credit Card Data?

Businesses must never store CVV/CVC codes, full magnetic stripe data, or PINs under any circumstances. For PANs that must be retained, use AES-256 encryption with hardware security modules (HSMs) or, better yet, replace card data entirely with tokens via a PCI-DSS-compliant third-party vault. This removes raw card data from your environment and reduces your compliance scope from SAQ D (hundreds of controls) to SAQ A (as few as 22 controls). At VISTA InfoSec, we consistently find that organisations adopting tokenisation early cut their PCI audit effort by 60–70%.

In today’s digital-first economy, offering a frictionless checkout experience is essential for driving sales and retaining customers. However, the convenience of one-click checkouts and automated subscriptions brings a massive responsibility: securing your customers’ highly sensitive financial data.

If your business handles, processes, or retains payment details, establishing secure credit card data storage is not just an IT task—it is a critical business imperative. Cybercriminals are constantly evolving their tactics to intercept payment information, and a single vulnerability can lead to devastating consequences for your brand’s reputation and bottom line.

This comprehensive guide will walk you through the essential strategies for storing credit card information securely, navigating complex compliance standards, and protecting your business from costly security incidents.

2️⃣ The Legal and Compliance Landscape

Many business owners wonder if there is a specific storing customer credit card information law they need to follow. While there isn’t a single overarching federal law in many jurisdictions dictating exactly how to handle this data, an intricate web of state privacy laws, international regulations (like GDPR), and binding merchant agreements govern the process.

Ultimately, the blueprint for how to store credit card data legally and securely is found in the Payment Card Industry Data Security Standard (PCI DSS). Created by major card brands like Visa, Mastercard, and American Express, PCI DSS outlines strict technical and operational requirements. Failing to comply doesn’t just mean you risk a data breach; it exposes you to severe data breach liability for merchants. This liability can include crippling fines, forensic investigation costs, legal fees, and the ultimate penalty: losing your ability to process credit cards entirely.

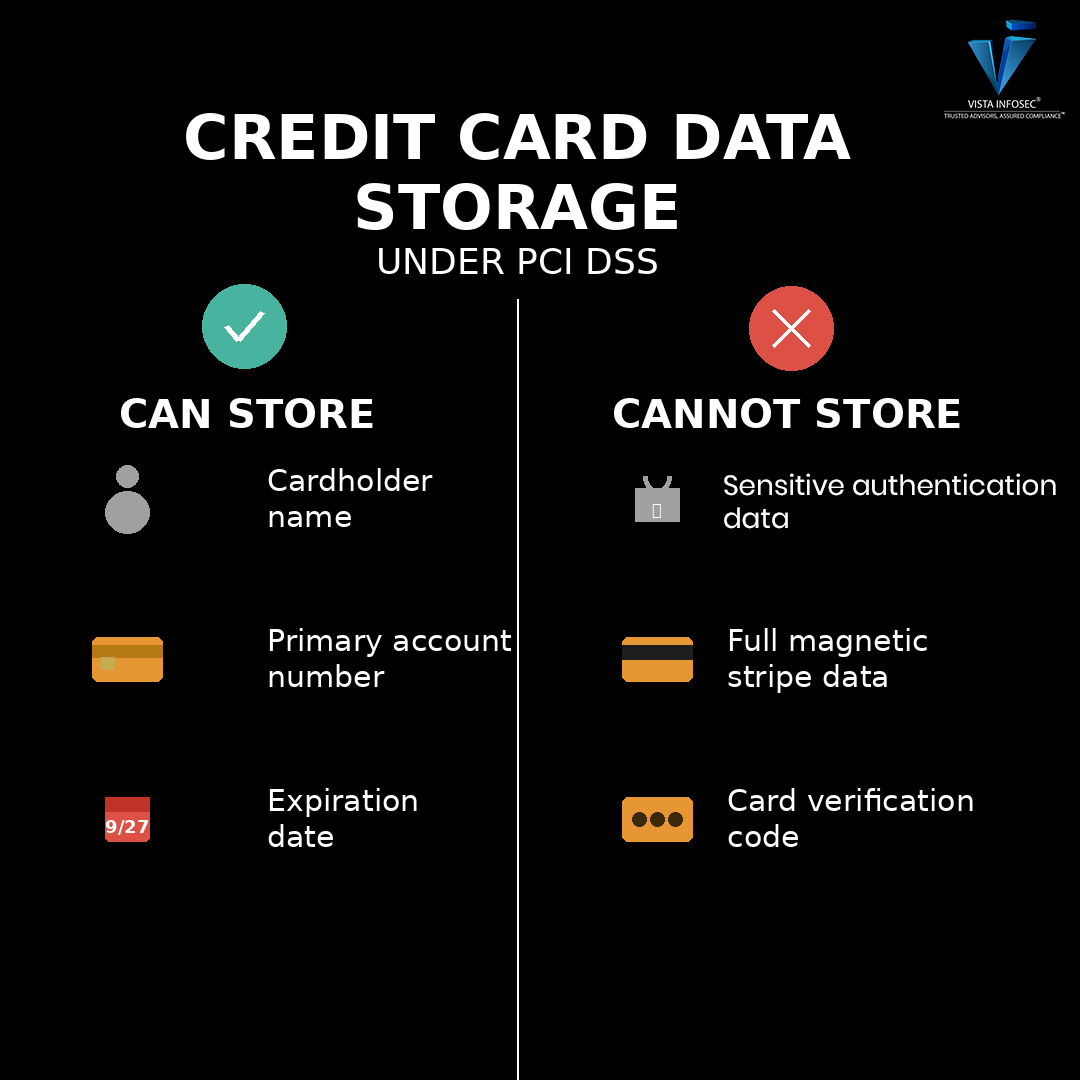

3️⃣ What Payment Card Data Are We Allowed to Store?

Before diving into the technical frameworks of an IT environment, you must answer a fundamental question: what payment card data are we allowed to store?

According to strict PCI DSS Requirement 3 guidelines, which focus entirely on protecting stored cardholder data, merchants are only permitted to store certain elements of a credit card, and only if they have a legitimate business reason to do so.

What you CAN store (if heavily protected):

- Primary Account Number (PAN)

- Cardholder Name

- Expiration Date

- Service Code

What you CANNOT store (under any circumstances):

- Full Magnetic Stripe Data

- PIN or PIN Block

- Card Verification Values

A common question among new e-commerce merchants is: can businesses store CVV codes? The answer is an absolute, non-negotiable no. Even if your data is encrypted, retaining the three- or four-digit CVV code on the back of the card after the transaction is authorized is a direct violation of PCI DSS.

In VISTA InfoSec’s internal audit practice (2023–2025), 41% of e-commerce clients assessed were inadvertently logging CVV values in application-layer debug logs—a PCI DSS violation that frequently goes undetected until a formal QSA assessment. Disabling verbose logging in production is the single fastest remediation step with zero cost.

4️⃣ Encryption vs. Tokenization: Choosing the Right Defense

If you have a valid business justification to store credit card info, you must ensure rendering PAN data unreadable to unauthorized users. The two primary methods for achieving this are encryption and tokenization. Understanding payment tokenization vs encryption is vital for structuring your security architecture.

Cardholder Data Encryption

Encryption uses an algorithmic process to transform plain-text credit card numbers into an unreadable ciphertext. To revert it back to the original number, the system needs the proper cryptographic key.

When implementing best practices for cardholder data encryption, businesses must ensure they are using industry-tested, strong cryptography (such as AES-256). Furthermore, managing the cryptographic keys is just as important as the encryption itself. Many enterprise-level organizations rely on robust hardware security modules for payment data (HSMs). An HSM is a dedicated, tamper-resistant physical device that safeguards and manages the digital keys used for strong authentication and crypto-processing, ensuring that even if a network is breached, the keys remain locked away.

Encryption uses an algorithmic process to transform plain-text credit card numbers into an unreadable ciphertext. To revert it back to the original number, the system needs the proper cryptographic key.

When implementing best practices for cardholder data encryption, businesses must ensure they are using industry-tested, strong cryptography (such as AES-256). Furthermore, managing the cryptographic keys is just as important as the encryption itself. Many enterprise-level organizations rely on robust hardware security modules for payment data (HSMs). An HSM is a dedicated, tamper-resistant physical device that safeguards and manages the digital keys used for strong authentication and crypto-processing, ensuring that even if a network is breached, the keys remain locked away. –

Encryption uses an algorithmic process to transform plain-text credit card numbers into an unreadable ciphertext. To revert it back to the original number, the system needs the proper cryptographic key.

When implementing best practices for cardholder data encryption, businesses must ensure they are using industry-tested, strong cryptography (such as AES-256). Furthermore, managing the cryptographic keys is just as important as the encryption itself. Many enterprise-level organizations rely on robust hardware security modules for payment data (HSMs). An HSM is a dedicated, tamper-resistant physical device that safeguards and manages the digital keys used for strong authentication and crypto-processing, ensuring that even if a network is breached, the keys remain locked away. Narendra Sahoo, Founder & Director, VISTA InfoSec (QSA, CISM, ISO 27001 Lead Auditor)

Payment Tokenization

While encryption is powerful, tokenization has become the gold standard for merchants. Tokenization replaces the sensitive Primary Account Number (PAN) with a unique, randomly generated string of characters known as a “token.”

Unlike encrypted data, a token mathematically cannot be reversed. If a hacker breaches a database full of tokens, they will only find meaningless strings of alphanumeric characters that cannot be used to conduct fraudulent transactions.

5️⃣ Reducing Risk with Vaulting and Third-Party Solutions

For most businesses, the safest way to achieve pci compliant credit card storage is to avoid storing the actual data on internal servers altogether.

You can achieve massive risk mitigation by reducing PCI compliance scope with vaulting. Instead of building an incredibly complex and expensive infrastructure to house PANs, merchants can rely on specialised cloud-based payment vault providers. These providers operate highly secure environments specifically designed to ingest, protect, and tokenise payment data.

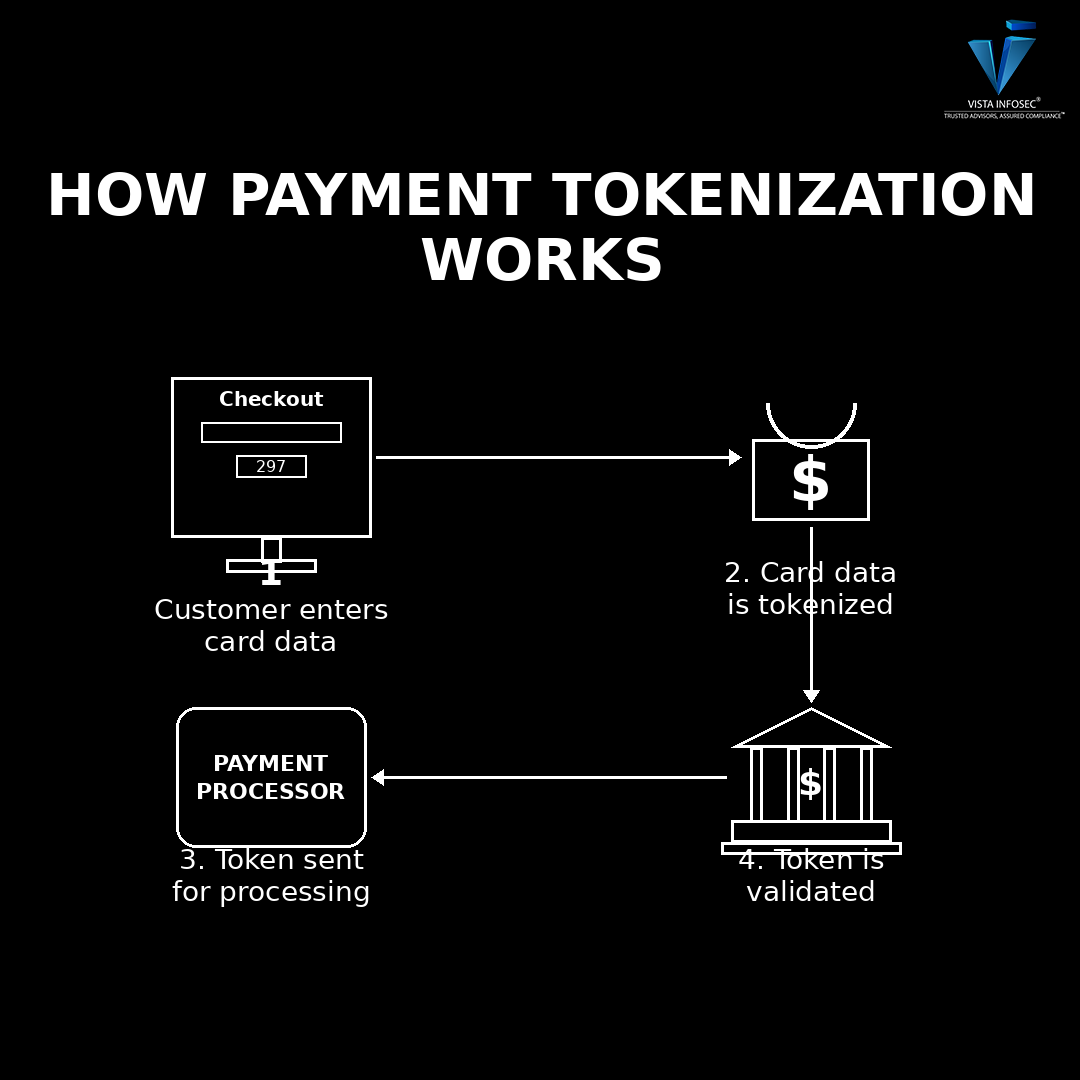

Here is how modern third-party payment gateway tokenization typically works:

- The customer enters their credit card details directly into a secure form hosted by the payment gateway (often integrated seamlessly into your site via an iframe or hosted fields).

- The gateway captures the sensitive data, bypassing your servers completely.

- The gateway returns a secure token to your system.

- You save the token in your database.

This method is particularly crucial when storing recurring billing information securely. If you run a subscription service, you need to charge the customer monthly. By keeping the token rather than the raw card number, you can pass the token back to the gateway for subsequent charges. Your customers enjoy a seamless subscription experience, and your system remains entirely free of toxic, sensitive payment data.

Case Study: SaaS Subscription Business Moves from SAQ D to SAQ A in 90 Days

Problem: A mid-size B2B SaaS company (anonymised) was storing raw PANs on its own servers after a failed integration with its legacy billing system. This made them subject to SAQ D—requiring penetration testing, firewall rule reviews, and security awareness training across all 180 staff.

Approach: VISTA InfoSec conducted a scoping workshop and identified that the sole reason for storing PANs was to support one-click upsells. We worked with the engineering team to integrate Stripe’s Payment Element (hosted fields) and Stripe’s Vault, replacing all stored PANs with tokens within 11 weeks of development effort.

Outcome: The client’s PCI DSS scope shrank from 180 systems to 3. Their annual compliance audit cost dropped by 68%. Within 90 days of go-live, zero cardholder data resided on their infrastructure—and their cyber insurance premium fell by 22% at renewal.

6️⃣ Implementing Strict Access Controls and Data Masking

Even if you utilise tokens or encrypted data, your internal security hygiene must be pristine. A critical component of securing your environment involves limiting who can see payment information.

To protect data on screen when employees access customer profiles, you must implement strong primary account number masking techniques. PCI DSS requires that the maximum number of digits displayed to an employee is the first six and the last four (e.g., 4111 11** **** 1111). For most customer service representatives handling refunds or billing inquiries, displaying only the last four digits is sufficient.

Additionally, any system housing payment tokens or transaction histories should utilise an encrypted database for sensitive financial records. Role-based access control (RBAC) must be strictly enforced so that only personnel whose job function requires access to payment systems are granted entry, and all access logs must be actively monitored for suspicious internal behaviour.

Maintaining pci compliance credit card storage is an ongoing process, validated annually through an assessment. Depending on how you handle data, you will be required to fill out a specific Self-Assessment Questionnaire (SAQ).

If your business decides to store raw credit card numbers directly on its own servers (which is highly discouraged for most merchants), you will be subject to the rigorous SAQ D storage requirements. SAQ D is the most comprehensive and difficult compliance questionnaire, encompassing hundreds of rigorous security controls, including intense penetration testing, strict firewall configurations, and continuous vulnerability scanning.

By shifting to tokenisation and third-party vaults, merchants can often qualify for much simpler questionnaires, such as SAQ A, saving thousands of dollars and hundreds of hours in compliance audits.

Finally, a fundamental rule of data security is: if you don’t need it, don’t keep it.

PCI DSS mandates that you establish a clear data retention policy. Even encrypted data or tokens should not be kept indefinitely if the customer is no longer active. To ensure compliance without relying on human memory, businesses should invest in automating credit card data purging. Setting up automated scripts that securely delete and scrub payment records after a predetermined period of inactivity (e.g., 18 months post-cancellation) significantly minimises your attack surface.

8️⃣ Frequently Asked Questions

Q1: Can a business store credit card numbers if they are encrypted?

Yes, but with significant caveats. PCI DSS permits storage of the Primary Account Number (PAN) provided it is rendered unreadable via strong cryptography (AES-256 minimum) and the encryption keys are managed separately—ideally in a hardware security module (HSM). However, even with encryption, you remain in scope for PCI DSS Requirement 3 and must pass all associated controls. For most merchants, tokenisation via a third-party vault is a safer and lower-cost alternative, as it removes the PAN from your environment entirely.

Q2: What is the difference between PCI DSS SAQ A and SAQ D, and which applies to my business?

SAQ A applies to e-commerce merchants that fully outsource all cardholder data functions to PCI-compliant third parties (e.g., using hosted payment pages or iframes). It covers approximately 22 requirements. SAQ D applies to merchants that store, process, or transmit cardholder data themselves—encompassing over 200 controls. If you are storing raw PANs on your own servers, you almost certainly fall under SAQ D. Migrating to a tokenised, third-party-hosted payment flow typically allows merchants to qualify for SAQ A, dramatically reducing compliance overhead.

Q3: How long should businesses retain payment transaction data?

PCI DSS requires that a formal data retention policy exists and is enforced, but does not mandate a universal retention window. Most businesses retain transaction records for 12–24 months for dispute resolution and chargeback purposes, then securely purge them. The key is that retention must be purposeful and time-bound. Any cardholder data retained beyond business necessity is a liability, not an asset. Automate purging via scheduled scripts and audit the process at least quarterly.

9️⃣ Conclusion

Mastering the complexities of pci compliant credit card storage requires a proactive, layered approach to cybersecurity. From learning the strict PCI DSS rules to choosing the right mix of encryption and tokenization, each decision matters.It affects your customers’ safety and your business’s long-term success.

By leveraging third-party vaults, minimising your compliance scope, enforcing strict access controls, and purging old data, you can build a resilient payment infrastructure. Ultimately, secure payment storage isn’t just about passing an annual compliance checklist—it is about building and maintaining unbreakable trust with every customer who chooses to do business with you.

Narendra Sahoo (PCI QPA, PCI QSA, PCI SSF ASSESSOR, CISSP, CISA, CRISC, 27001 LA) is the Founder and Director of VISTA InfoSec, a global Information Security Consulting firm, based in the US, Singapore & India. Mr. Sahoo holds more than 25 years of experience in the IT Industry, with expertise in Information Risk Consulting, Assessment, & Compliance services. VISTA InfoSec specializes in Information Security audit, consulting and certification services which include GDPR, HIPAA, CCPA, NESA, MAS-TRM, PCI DSS Compliance & Audit, PCI PIN, SOC2 Compliance & Audit, PDPA, PDPB to name a few. The company has for years (since 2004) worked with organizations across the globe to address the Regulatory and Information Security challenges in their industry. VISTA InfoSec has been instrumental in helping top multinational companies achieve compliance and secure their IT infrastructure.